Internal auditors uphold the spirit of transcendence and independence, with an objective and fair standpoint, truly perform their duties, and pay due professional attention. The audit supervisor regularly reports the audit results to the audit committee and the BOD.

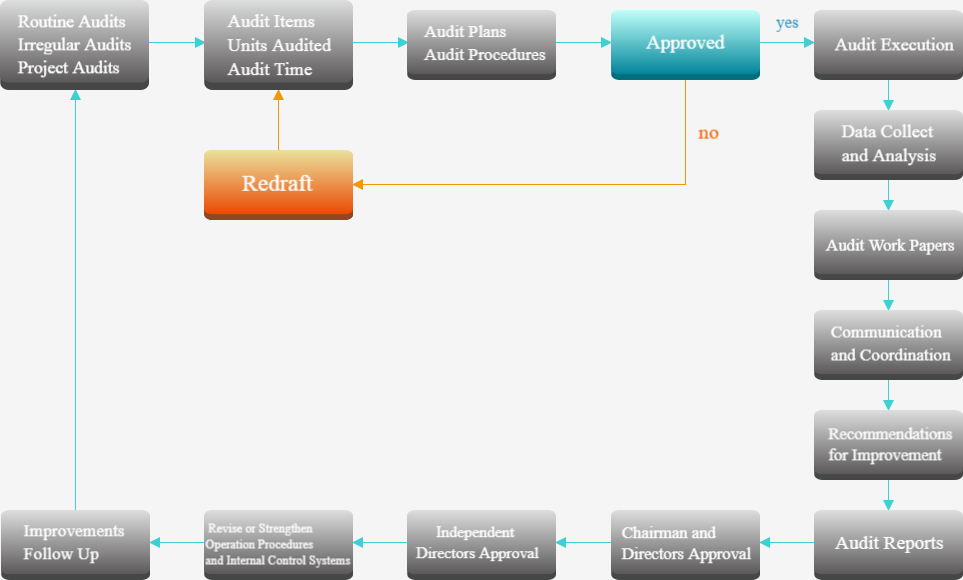

The internal audit operation of the company draws up an annual audit plan based on the results of the risk assessment, specifying the audit items, time, procedures and methods. Auditors conduct routine and project audits on a regular or irregular basis. The audit results are submitted with working papers and related materials to make audit reports for submission to ensure that the company's internal control system is continuously and effectively implemented.

Supervise the internal departments and subsidiaries of the company to evaluate the effectiveness of the internal control system on a regular basis each year. The self-evaluation supervisor of each department conducts the internal control system design and implementation effectiveness evaluation based on the internal control risk, and then the internal audit office reviews the self-assessment report of each department and subsidiary, and the improvement of internal control deficiencies and abnormal matters found by the internal audit office. All above will be the main basis for the BOD and the general manager to assess the effectiveness of the overall internal control system and to issue an internal control system declaration.

The internal auditors disclosed the defects and abnormalities of the internal control system found in the internal audit operations, listed in the internal control system declaration, self-assessment and accountant's project review, according to the facts in the audit report, and follow up after improvement and prepare quarterly follow-up reports to confirm that relevant units have taken appropriate improvement measures in a timely manner and list them as important items for the performance appraisal of each department. After the audit report and the follow-up report are reviewed, they shall be submitted to the audit committee for review before the end of the month following the completion of the audit project. If internal auditors discover major violations or the company is in danger of major damage, they shall immediately prepare a report and to notify the BOD and audit committee.